Michael McWalter writes about petroleum development in its widest sense, including the discovery and extraction of oil and gas resources from the ground to generate revenue, provide energy and feedstock, and the various roles and responsibilities of stakeholders and their interrelationships.

What is Petroleum Development?

In broad terms, petroleum development is the overall process of finding, extracting and refining oil and gas from the Earth, often collectively called petroleum, or more broadly hydrocarbons, though the latter term also includes coal.

Sometimes the term petroleum is used more strictly to refer to crude oil, derived from the Latin words petra, meaning rock, and oleum, meaning oil — hence “rock oil”. However, oil rarely occurs without associated gaseous hydrocarbons, which are often termed natural gas, or simply gas.

Some fields contain mainly gas and only a few of what are called wetter (liquid) hydrocarbons, which can be extracted from the gas, such as condensate and natural gas liquids. Papua New Guinea has some oil, but considerably more gas.

Once extracted, these substances have many uses, primarily as a source of energy, but also as feedstock for the petrochemical industry. Oil and gas therefore have significant economic value, and are regarded as resources with a market price once they are extracted, processed, and made ready for sale to customers.

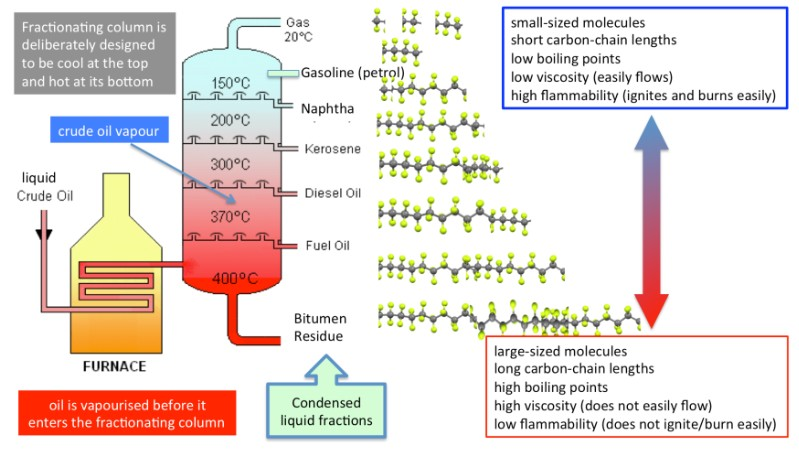

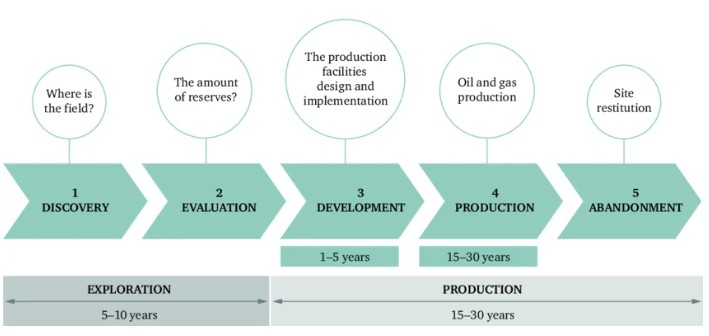

Petroleum resource development involves a complex and expensive process of exploration, drilling, discovery and appraisal, development and production, followed by the refining of produced petroleum fluids, traditionally through distillation and other processes to produce specification petroleum products with which we are all familiar.

In the case of oil, these typically include gasoline (petrol), kerosene, jet fuel, diesel, heating oil, solvents, lubricants, asphalt and paraffin wax. For gas, the products typically include reticulated gas, liquefied petroleum gas (LPG), or bottled gas, and piped natural gas or liquefied natural gas (LNG) for the long-distance transportation of natural gas.

There are also other products that are less commonly seen, such as heavy fuel oil, or those that serve as intermediate feedstocks, including naphtha, ethane and propane.

It All Begins With Exploration

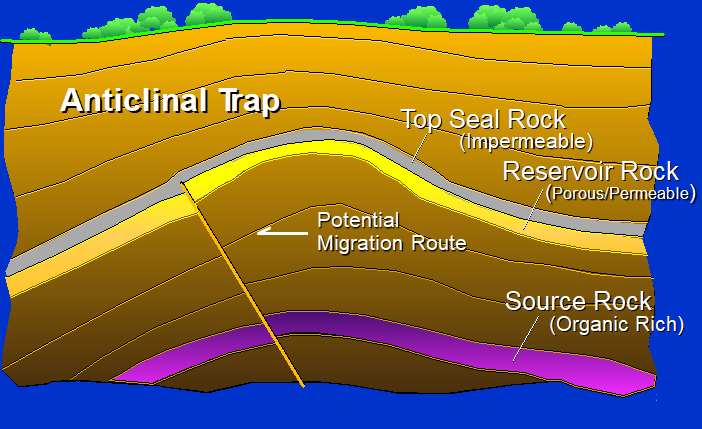

Exploration is an exhaustive, expensive and often high-technology process. It is predicated on the presence of essential geological ingredients that allow rock strata and their contents to form gaseous and/or liquid hydrocarbon accumulations in the Earth’s subsurface rocks.

The process develops over millions of years as organic matter contained in rock strata, buried beneath successive layers of overburden, is transformed by heat and pressure into oil and gas.

The key ingredients in this process are:

• An organically rich source rock which, when deeply buried and heated, generates petroleum;

• The movement of generated petroleum, driven by buoyancy, from the source rocks through rock strata until it becomes trapped in a reservoir rather than escaping to the surface;

• A reservoir rock with sufficient porosity (space between its grains) to store petroleum, and adequate connectivity between those pore spaces to allow petroleum to flow if tapped by a well drilled into the reservoir;

• A closure or trap formed by the structural configuration of rock strata, where folding, faulting or stratigraphic pinch-out creates a location in which petroleum can accumulate; and

• A seal or containment layer that acts as a barrier to the upward movement of petroleum, created by impermeable rocks or structures that prevent further migration and escape.

Papua New Guinea as a Petroleum Province

Papua New Guinea is not lacking in any of these ingredients. Indeed, the country’s geology is conducive to the formation of petroleum accumulations, although all the essential elements must occur in the correct sequence and at the right time. Such accumulations must also contain sufficient petroleum resources to make their development commercially worthwhile and capable of delivering what are known as recoverable reserves.

Across Papua New Guinea there are many surface seeps of oil and gas, which provide evidence of petroleum generation in the subsurface and its migration and seepage to the surface at discrete locations. While these seepages indicate the presence of oil and gas, they also show that hydrocarbons are leaking to the surface.

Petroleum explorers therefore look for accumulations that have been preserved intact deep within the rock strata, without such leakage, into which they may drill deep wells to tap oil and gas in commercially viable quantities.

Papua New Guinea also exhibits extensive folding and faulting of rocks, as well as the presence of suitable rock types — permeable and porous sandstones and limestones that can serve as reservoirs, and abundant mudstones and shales that can act as source rocks and seals.

The critical question, however, is where exactly to look for a petroleum accumulation.

The Value of Petroleum

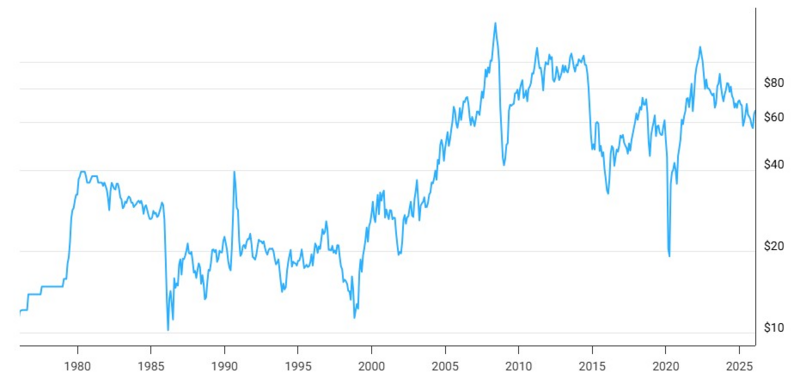

Oil and gas are not like gold. A barrel of crude oil — approximately 159 litres — currently (as of late February 2026) sells for about US$65, or PGK278. That equates to roughly 40 US cents per litre, or PGK1.75 per litre. A litre of crude oil is not going to make you rich.

By contrast, a litre of gold would weigh a staggering 19.3 kilograms (equivalent to about 620 troy ounces) and be valued at an equally staggering amount — about US$3.1 million, or PGK13.4 million — at a gold price of US$5,000 per troy ounce.

The petroleum business is therefore very different from the gold business. A small surface seepage of natural gas or oil has little economic value and is more a local curiosity.

The discovery of an accumulation of oil or gas must therefore be large and extensive to justify future development and recovery. Accordingly, petroleum explorers select their exploration prospects for what is termed wildcat drilling with considerable care and rigour.

Wildcat drilling refers to high-risk exploration for oil and gas in unproven, unmapped or abandoned areas lacking existing oil and gas production, or located far from producing fields, often without any historical discovery or prior production.

Explorers screen the geology of an area for the necessary ingredients described earlier, particularly large geological structures that may potentially contain significant volumes of oil and/or gas.

Oil Production Economics

Oil production from a field from which, say, 100 million barrels of crude oil can be recovered might, at a crude oil price of US$65 per barrel, have a sales value of about US$6.5 billion. However, not all of that revenue goes into the oil producer’s pocket.

For example, it might take five wells to make the discovery, a further five wells to appraise the lateral extent of the field, and another 30 wells from which the oil may ultimately be recovered. These 40 wells might cost an average of US$25 million each, bringing the total discovery and appraisal cost to about US$1 billion.

The development of the field would also require processing facilities to treat the crude oil to acceptable standards and specifications so it can be transported. It would likely also require a pipeline, or a network of pipelines, to convey the oil to a terminal where ocean-going tankers can load the crude oil for export. This infrastructure could cost another US$1.5 billion.

There are also operating costs. Running an oil field and producing crude oil safely and responsibly involves daily expenses for manpower, machinery and materials. These costs might amount to about US$100 million per year over a 20-year production life.

As these costs accumulate, the apparent prize of discovering the oil field begins to shrink.

In addition, the government will expect to receive its agreed share of the resource as the owner, typically at least 50% or more of the project’s net value. It is therefore easy to see how revenue from the production of 100 million barrels of oil can be significantly reduced after costs and government take are accounted for.

In such a scenario, oil companies might retain around US$1 billion from the project after recovering their costs, while the host government might receive a similar amount.

Naturally, every petroleum project has a different combination of reserves, costs and outcomes. Demonstrating that oil can be produced economically from a field is the primary consideration. Establishing a firm and fair arrangement for sharing the net value of the produced petroleum is also essential.

Exploration and Discovery Risk

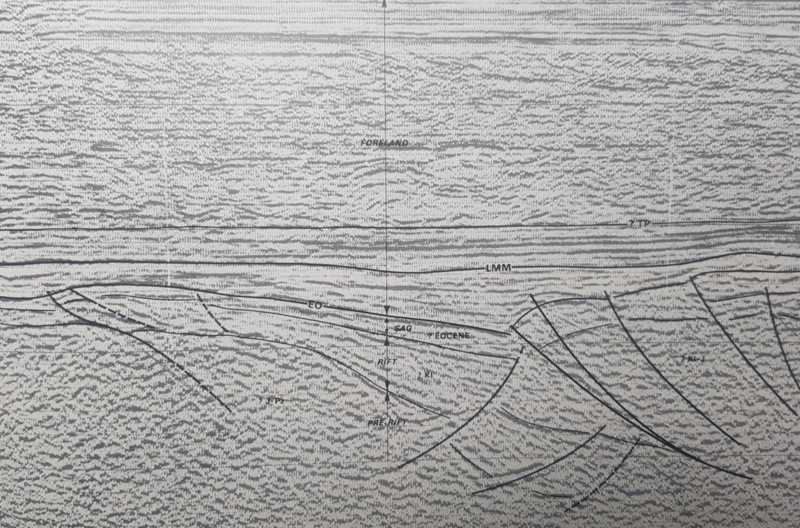

Exploration drilling only takes place after extensive and expensive surveys conducted by geologists and geophysicists studying rock formations at the surface and investigating the subsurface using various geophysical techniques.

The most common technique is seismic surveying, which produces images of the subsurface in a manner somewhat similar to a medical ultrasound scan, although on a vastly larger scale. Sound waves are transmitted into the ground — or into the seabed in offshore exploration — and reflections from layers of rock are recorded by numerous specialised sensors known as geophones.

These signals are then organised and processed by sophisticated computer programmes to create a layered image of the structure of subsurface rock formations.

By analysing the velocity of sound travelling through different rock layers, geophysicists can interpret these seismic images and construct depth maps of potential trapping structures.

This is a tedious and expensive process, particularly in the jungle-covered, mountainous and often swampy terrain that characterises much of Papua New Guinea.

Combined with surface geological mapping of exposed rock formations and their faulting and folding, petroleum geologists attempt to identify leads and prospects that may later be selected for wildcat drilling.

Even at this stage, tens of millions of dollars may already have been spent on field surveys, data processing and geological and geophysical interpretation.

The company must then evaluate its portfolio of prospects, both within the country in which it is exploring and globally, and decide which prospects in which countries it will prioritise and commit to drilling. This assessment is conducted on a risked basis, after which the company applies the economics of the relevant national petroleum regime to determine whether the project could potentially be profitable.

The petroleum business is inherently risky, somewhat akin to producing an expensive film that may ultimately succeed or fail. Some observers compare it to gambling in a casino because of the intrinsic uncertainty of subsurface geological history. However, oil and gas companies carefully assess and manage the many risks involved.

Drilling the Ultimate Gamble

There are fundamental geological uncertainties about whether a petroleum accumulation is present within a given prospect. Ultimately, the only way to determine whether a prospect contains oil or gas is to drill it.

The probability of discovery varies depending on the type of well. Success rates for wildcat exploration wells typically range from 10% to 20% in new frontier areas, compared with a global average of about 30% to 40%.

In practical terms, roughly 60% to 70% of initial exploration wells fail to discover accumulations in quantities sufficient for commercial development and production.

In established petroleum provinces, where development drilling takes place near or within known accumulations, success rates can be much higher, typically between 80% and 90%. As a result, petroleum provinces in long-established producing countries generally present significantly lower exploration risk than previously undrilled regions where little or no drilling has taken place.

The risk of discovery is influenced by perceptions of a host nation’s petroleum endowment. As a result, governments often adjust the terms and conditions for petroleum development depending on the likelihood of discovery.

Drilling a wildcat well in the Seychelles, where only four wells have previously been drilled without success, is very different from drilling a wildcat well in Libya, where more than 1,500 wells have been drilled over the past 70 years, resulting in more than 500 oil and gas discoveries. Consequently, the government of the Seychelles may need to offer more attractive fiscal and contractual terms to encourage international oil and gas companies to explore within its territory rather than in other, potentially more petroliferous regions.

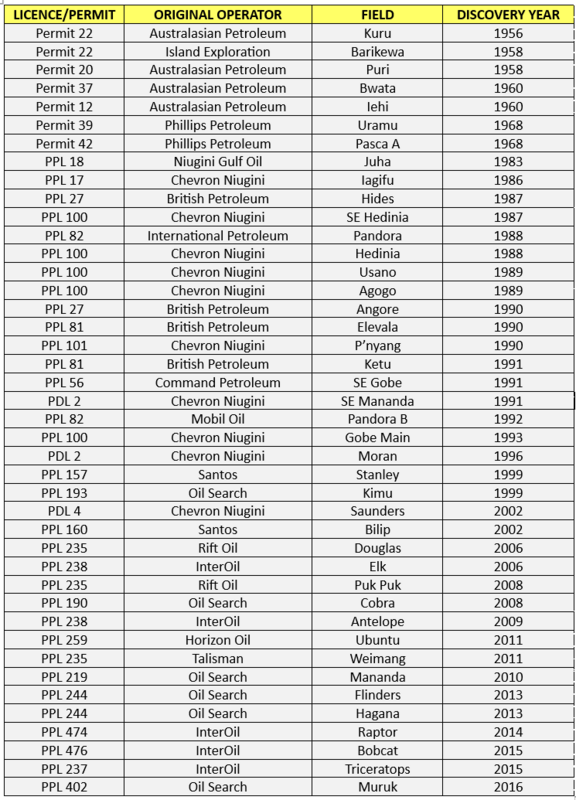

In Papua New Guinea, fewer than 275 genuine wildcat wells have been drilled over the past century. The Wohumul boreholes were drilled in the Oriomo River area of Western Province, near Daru, in 1925, although these were shallow tests.

The first deep well in Papua New Guinea was drilled at Kariava-1 in Gulf Province. Notably, this well was spudded on March 8, 1941, suspended in 1942 due to World War II, and drilling resumed in 1946 before the well was abandoned in 1948.

Exploration for oil in Papua New Guinea is therefore not new. It has taken place for decades, producing tantalising results that have intrigued many petroleum explorers.

Significant success was finally achieved in 1986 with the Iagifu 2-X well, when Niugini Gulf Oil — later incorporated into Chevron Corp. as Chevron Niugini — discovered a major accumulation of crude oil near Lake Kutubu. This discovery led to the Kutubu Petroleum Development Project in 1990.

Before that discovery, no commercially significant oil or gas accumulation had been developed in Papua New Guinea. Since then, oil and gas have been discovered in dozens of prospects across the country, at least half of which have progressed to development and production, yielding crude oil and natural gas in commercially viable quantities.

Factors Affecting Petroleum Development

Finding an accumulation of oil and/or gas is a great moment for petroleum explorers. However, unless the volume of the accumulation is large enough to be commercially exploited through development and production, it cannot compensate a company for the considerable expense incurred in discovering it.

The cost of drilling a well depends greatly on its location and its distance from supply chains and support facilities. Papua New Guinea remains a remote location for petroleum development operations of all kinds, being far from major petroleum industry hubs. Much of the country still qualifies as a frontier petroleum province, despite 34 years of crude oil production and 12 years of gas production and liquefied natural gas (LNG) exports.

Put simply, Papua New Guinea is not Texas, where more than 1.5 million wells have been drilled and between 157,000 and 187,000 wells remain active. The presence of extensive civil and petroleum infrastructure in Texas significantly lowers the cost of petroleum development.

Although high-production wells dominate output today, thousands of older “stripper wells” across Texas produce fewer than 10 to 15 barrels per day. Even such modest production can generate reasonable income if privately owned and if the crude oil can readily reach the market through a nearby pipeline. The situation in Papua New Guinea is very different, where civil infrastructure is limited and petroleum infrastructure is typically project-specific and sparse.

A frontier province is an unexplored or underexplored geological region with suspected, but unproven, petroleum resource potential. This is the case in the deep waters of the Coral Sea, where TotalEnergies and Petronas plan to drill the Mailu-1 deepwater well, targeting Eocene carbonate reservoirs.

Such a deepwater well is likely to cost about US$100 million, with an estimated drilling period of less than two months. These risks are not for the faint-hearted. It has often been said that drilling a true wildcat well in a basin where no prior exploration drilling has taken place is somewhat like entering a casino for the first time and bypassing the slot machines to go straight to the high-stakes tables.

Of course, it is not always certain whether a sedimentary basin contains petroleum accumulations or has even generated oil and gas. Sometimes the subsurface conditions are simply not suitable, or the necessary geological elements did not develop in the correct sequence. In other cases, there may be no indication of oil or gas seeping to the surface.

In such situations, exploration can resemble a blind gamble. However, once a discovery is made in a newly explored basin, other oil and gas companies often quickly follow.

Achieving that crucial first discovery is therefore extremely important — not only for the company undertaking the exploration, but also for the host government, which seeks to fully understand and develop the country’s petroleum potential.

The Government Role

Many governments around the world shy away from anything beyond the most basic oil and gas exploration activities because of the considerable expense and enormous risks involved. They may commission seismic reflection surveys, particularly in offshore areas, either through bilateral assistance or through speculative surveys conducted by seismic contractors.

In such cases, the contractor finances the survey and then markets the resulting data to oil and gas companies, typically providing the host government with a royalty or profit share. These surveys can stimulate exploration interest from established petroleum companies and generate scientific interest within academia, as they provide new geological insights into the subsurface.

Governments typically offer unexplored areas for exploration by competent oil and gas companies through licences or contractual arrangements. Competence in this context extends beyond technical capability and includes corporate governance, environmental management, financial strength, safety performance and social responsibility. All of these capacities are required at different stages of the petroleum development cycle.

For these reasons, host governments often engage international oil and gas companies, which possess the necessary expertise and experience. However, governments must also hold these companies strictly accountable. Where deficiencies arise, sanctions and penalties should be applied.

A host government must therefore rise to the challenge of regulating the companies it licenses or contracts by maintaining a highly capable petroleum regulatory institution. The staff of such institutions should be well trained and appropriately compensated, as they serve as custodians of the nation’s oil and gas resources.

Government objectives are primarily economic: to convert the value of petroleum resources into revenue that can support national development. At the same time, governments often seek greater visibility into petroleum operations. As a result, many choose to participate directly in development and production by taking an equity stake in petroleum projects.

Papua New Guinea, for example, has the legal option to acquire up to a 22.5% participation interest in petroleum projects. This provides the government with valuable insight into project development as well as an additional source of revenue.

There are also broader policy objectives associated with petroleum development. For many countries, ensuring the security of domestic energy supply is a key priority. At the same time, governments often seek to maximise the participation of local businesses and workers in the petroleum industry.

Encouraging local employment, contracting domestic companies and developing local supply chains are therefore important policy goals. Achieving these objectives should not merely be a political aspiration but rather a coordinated effort between government and industry, supported by appropriate incentives and capacity-building initiatives.

Exploration Commitments

Investing companies normally bear the costs of basic exploration and are required to conclude their exploration programmes by identifying prospects where petroleum accumulations may have formed and drilling wells to test whether hydrocarbons are present.

These agreed exploration programmes constitute the companies’ work commitments to the host government. Failure to undertake and complete the required work typically results in the cancellation of the licence or contract.

In some cases, companies withdraw from an exploration area for various reasons. They may be unable to identify structures that justify the considerable expense of drilling. There may be insufficient evidence suggesting the presence of petroleum accumulations, or the company may identify more attractive prospects in other areas it is exploring, either within the same country or elsewhere.

Oil and gas companies generally maintain a global portfolio of exploration areas, seeking to balance overall exploration risk while prioritising the drilling of their most promising prospects.

If a company cannot fulfil its work programme, it must normally relinquish the area and return it to the government, sometimes with penalties. This allows the host government to offer the area to another company that may bring different ideas, geological interpretations or a greater appetite for exploration.

What governments seek to avoid is companies holding prospective areas without undertaking meaningful exploration work, hoping that discoveries in adjacent areas will increase the value of their own acreage. Such behaviour amounts to speculation and runs counter to the purpose of granting licences or contracts for legitimate exploration activity.

When a new petroleum province opens following a significant discovery, the oil and gas industry often responds quickly, with many companies seeking to secure exploration opportunities. Governments should take advantage of this momentum to encourage further exploration investment.

Indeed, the most compelling indicator of the potential for additional discoveries is the presence of nearby discoveries, which often enhance the perceived prospectivity of surrounding areas. Governments therefore need to remain agile in promoting their petroleum resources for exploration and development.

Petroleum Rights

Except on private lands in the United States, petroleum rights around the world are generally owned by the sovereign government of the host country. The United States is unusual in that subsurface mineral rights on private land are often tied to surface ownership, although the federal government retains control over mineral resources on federal lands and in offshore areas.

In most jurisdictions, therefore, the government owns the petroleum resources that exist beneath the ground. By allowing oil and gas companies to explore for these resources, governments must ensure they receive an appropriate share of the value created from their development.

Oil and gas companies typically bear the cost and risk of exploration. If exploration efforts fail, the companies absorb the loss and leave empty-handed.

Following the discovery of recoverable crude oil at Kutubu in 1986, numerous oil and gas companies acquired exploration licences in Papua New Guinea. However, only a few ultimately made successful discoveries.

Among the companies that explored in Papua New Guinea but departed without major discoveries were Conoco, Shell, Phillips, Pennzoil, Statoil, Mobil, Amoco, Marathon, Petrofina, Santos, Woodside and Union Texas Petroleum, along with many smaller companies.

Some companies succeeded in certain areas but not in others. Others sold their interests in discoveries before development began, lacking the commitment, resources or strategic interest to continue through to production. Some companies entered the country, exited and later returned again, reflecting the highly mobile and opportunistic nature of exploration investment.

It is also important to remember that petroleum exploration rights are typically exclusive within a defined licence area or tenement and are granted for a limited period, after which they expire unless renewed or converted into development rights.

The Petroleum Regime

Petroleum rights are typically licensed or contracted to competent companies by a host government under defined terms and conditions set out in laws, regulations, contracts and licences. However, the real substance of these terms and conditions generally comes into effect only after a discovery has been made.

If companies are successful and identify accumulations worthy of commercial development, they become subject to fiscal regimes that require them to share a substantial portion of the value generated with the host government.

Petroleum regimes represent a fundamental exercise of national sovereignty over petroleum resources. These resources only acquire significant economic value when they can be recovered in sufficient quantities as recoverable reserves. Oil and gas remaining underground have little economic value unless they can be produced and sold in the market.

It is therefore the value of the produced petroleum that forms the basis of most petroleum fiscal regimes.

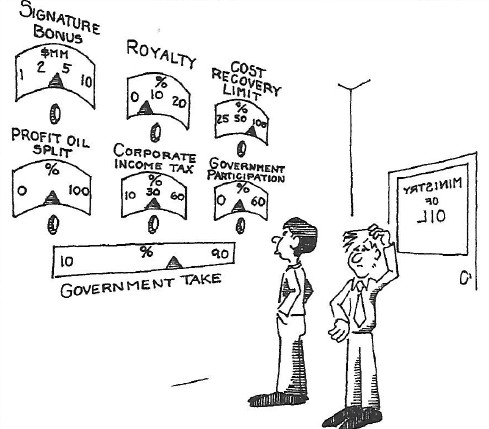

Governments have many mechanisms available to capture value from petroleum development. These may include rents, royalties, levies, bonuses, duties and fees; corporate income taxes; employee income taxes; withholding taxes on interest payments and dividends; government equity participation in petroleum projects; production-sharing arrangements; domestic supply obligations at discounted prices; and local content requirements.

These provisions are normally established through legislation, contracts, agreements and licence conditions before exploration begins and certainly before production operations commence. Establishing the fiscal framework in advance provides certainty for both the investing oil and gas companies and the host government.

Fiscal design should ideally account for a wide range of possible outcomes. In practice, however, precedent and political pressures sometimes distort clear economic decision-making.

The broad objectives of a petroleum regime are to reduce uncertainty, present a clear picture of the applicable commercial and tax terms, limit negotiations on tax issues, provide fair and equitable tax treatment for all investors, avoid double taxation, and ensure that international oil and gas companies can obtain home-country foreign tax credits for taxes paid overseas.

A general rule is that the more attractive the resource base, the tougher the fiscal and commercial terms imposed by the host government tend to be. However, many other factors also influence these terms, not least the remoteness of the location.

Take, for example, the Falkland Islands. Despite the discovery of oil in 2010, companies only reached a final investment decision for the Rockhopper oil field in late 2025, with first oil planned for 2028. The islands’ remoteness from supply chains — particularly specialised oilfield supply chains — as well as concerns about the Falklands’ ability to remain unaffected by Argentina’s territorial claims, contributed to the lengthy delay in progressing field development.

Papua New Guinea faces similar challenges related to remoteness, with Singapore and certain locations in Australia serving as the nearest supply bases for oil and gas operations. In addition, exploration activity has been insufficient to keep drilling rigs and other specialised equipment permanently stationed in Papua New Guinea. As a result, such equipment must often be imported repeatedly for individual exploration campaigns.

Access to Land

Papua New Guinea also remains an underexplored frontier oil and gas province with relatively low exploration density, although exploration efforts have achieved reasonable success in locating oil and gas accumulations. The country remains attractive for exploration due to clear evidence of significant oil and gas generation.

As in many parts of the world, local conditions also influence petroleum development. In Papua New Guinea, adherence to customary land tenure means that although the state asserts ownership of subsurface oil and gas resources, both the government and petroleum companies must obtain access to exploration areas by negotiating with local landowners.

Land ownership in Papua New Guinea is typically undocumented, inalienable and enduring under customary law. Consequently, both the state and petroleum companies must engage with landowners carefully and respectfully when seeking access to land for exploration and development activities.

The hopes and expectations of landowners naturally increase when oil and gas are discovered on their land. If a discovery is large enough to justify development and eventual production, customary landowners will inevitably be affected.

In Papua New Guinea — unlike in some jurisdictions where landowners may be forcibly removed — there are legally defined mechanisms through which landowners may participate in and benefit from petroleum development. Even during the exploration stage, oil and gas companies are required to pay compensation for entering or occupying land.

Companies must also conduct social mapping and landowner identification studies to ensure they are engaging with the appropriate customary landowners. By law, neither party is permitted to interfere with the rights of the other.

Companies have the legal right to enter and occupy land reasonably required for petroleum operations, but they must minimise disruption to existing land use and may not interfere with fishing or navigation. Landowners, for their part, are prohibited from entering or interfering with land that is being used for petroleum operations. These provisions establish both rights and responsibilities for each party.

When development begins, companies are encouraged to employ as much local labour and local content as possible. The government also provides business development grants to help local communities participate in project-related economic activities.

Although national content has been prominently emphasised in Papua New Guinea’s policy discussions in recent years, provisions requiring domestic procurement have existed in the Oil and Gas Act 1998 for nearly three decades. These provisions require companies to procure goods and services produced or supplied in Papua New Guinea whenever they can be obtained on comparable terms.

They also encourage companies to support citizens who wish to establish businesses supplying goods and services to the petroleum industry and to make maximum use of Papua New Guinean contractors and subcontractors.

However, these provisions have not always been strongly enforced. In many cases, regulations necessary to implement them fully have not been developed, and compliance by companies has rarely been systematically assessed.

The Oil and Gas Act also defines benefits for landowners, as well as for affected Local Level Governments and Provincial Governments, when petroleum projects move into production.

These benefits may include royalty payments, equity participation, development levies, project-related benefits and project grants. While the Act broadly identifies the categories of beneficiaries, the distribution of these benefits must still be negotiated.

For this reason, the legislation requires the government to convene a development forum, where representatives of all relevant stakeholders are invited to participate. Although this process can be complex and time-consuming, it represents a far more inclusive approach than is seen in many petroleum-producing countries.

Papua New Guinea can therefore take some pride in this legally established framework for consultation and benefit-sharing. Nevertheless, it must be implemented carefully and responsibly.

Changes to the petroleum regime — or uncertainty regarding its application — can also introduce additional risks for exploration and development. Governments naturally seek to maximise the value obtained from petroleum resources for the benefit of the nation.

At the same time, the fiscal and regulatory framework must allow companies to achieve a reasonable return on their investments. Striking this balance can be challenging.

When the balance cannot be achieved, exploration activity may decline, or the development of discovered resources may not proceed. Projects cannot move forward if the interests of both the government and the investors are not aligned.

Moreover, decisions regarding development are always based on assumptions about future market conditions and project performance, which remain inherently uncertain.

Production Risks

Production forecasts are developed through rigorous assessments of the amount of oil and gas that can potentially be recovered from a reservoir.

Well tests are conducted to evaluate how reservoirs behave and how much oil and gas individual wells can produce. The results of these tests are combined with geological analysis to prepare a field development plan and an associated production profile.

This plan typically outlines the number of development wells required to exploit the reservoir and the expected production over time. If sufficient appraisal drilling and geological analysis have been conducted, it becomes possible to estimate the proportion of oil and gas that can ultimately be recovered.

However, only a fraction of the oil and gas originally in place can be extracted. Recovery factors vary widely between fields, depending on reservoir characteristics, fluid properties and the way the reservoir depletes during production.

Some fields perform better than expected, while others fail to meet initial forecasts. These uncertainties must therefore be carefully managed.

Petroleum engineers and geologists work to reduce such risks, but they can never eliminate them entirely. In reality, the exact amount of oil and gas that can be recovered from a field is only known at the end of its economic life — when the value of production no longer covers the cost of extraction.

Even then, technical risks may be overshadowed by external factors. Oil and gas must reach international markets to generate value, and this can be affected by geopolitical or logistical disruptions.

For example, the closure of critical shipping routes such as the Strait of Malacca between Indonesia and Malaysia, or the Strait of Hormuz between Iran, the United Arab Emirates and Oman — through which roughly 20% of global oil supply passes — could severely disrupt petroleum trade.

Price Risks

The economic outcome of petroleum production is determined by the volume of oil and gas produced and the sale price per unit of production. That price depends on the quality of the oil and gas and prevailing global market prices for commodities of that quality. Natural gas is often priced with reference to crude oil benchmarks.

Importantly, the sales price for oil and gas is realised only after the produced hydrocarbons have been processed into saleable and transportable streams. Crude oil must be separated from water, sediment and associated gases. Similarly, natural gas must be conditioned to meet commercial specifications by removing water and impurities such as carbon, nitrogen and sulphur oxides, as well as extracting natural gas liquids that can be sold separately.

These processing steps involve significant cost but are necessary to ensure that the oil and gas can be transported safely by pipelines and ships and delivered to customers for further downstream processing and supply.

The price of oil is widely known to fluctuate significantly in global markets. Prices are influenced by a range of factors, most notably global supply and demand. Political developments, geopolitical tensions and international relations also play a major role. In recent years, energy transition policies have also begun to influence market expectations, although to a lesser degree.

Because oil and gas prices are inherently volatile, the projected revenues from any petroleum development project are also uncertain. Companies investing in such projects must therefore account for the risk of falling commodity prices, just as they must consider the potential benefits of higher prices.

Development projects must be capable of withstanding fluctuations in oil and gas prices over time. Since most petroleum projects operate for several decades, they must also take into account broader economic variables such as inflation, financing costs and the cost of capital, often represented in project economics by the discount rate.

Price Volatility and Fiscal Adjustment

These external factors can often overshadow the technical potential and forecast outcomes of a petroleum project. Oil and gas price behaviour, together with the value of money over the life of a project, are therefore critical considerations for both the investing company and the host government.

Regardless of the specific petroleum regime adopted, there must be a shared understanding of how fluctuations in commodity prices and changes in the value of money will affect project economics. Without such understanding, either party may be unfairly disadvantaged over the life of the project.

Most petroleum fiscal regimes therefore incorporate mechanisms that adjust how the net value of production is shared after the costs of exploration, development and production have been recovered.

For example, income tax is typically levied on net income or profit. If oil and gas prices decline, profits also fall and tax revenues decrease accordingly. In production-sharing arrangements, the division of production generally occurs only after companies recover their exploration and development costs. As a result, when prices fall, the company’s share — and the government’s share — also decline.

Fiscal systems may include additional adjustment mechanisms designed to accommodate both favourable and adverse market conditions. Royalty rates and other direct levies may be structured to scale with production or price levels. Capital depreciation allowances used for tax purposes may also be adjusted over time.

At the same time, windfall taxes, additional profit taxes or increased government production shares may be triggered during periods of exceptionally high commodity prices.

The key principle is that both parties — government and investor — must respect the long-term viability of the project and accommodate price volatility by recognising the legitimate interests of the other.

Other Development Criteria

When preparing a petroleum project for development and production, many additional considerations must be addressed.

Fiscal and commercial arrangements with the host government must be firmly established and robust under a range of possible economic outcomes. Environmental protection and the welfare of communities affected by the project must also be taken into account.

Petroleum development inevitably has social and environmental impacts, but these can be reduced through responsible planning and adherence to good operational practices.

While exploration and appraisal costs are typically financed through company equity, the much larger costs associated with development usually require borrowing from financial institutions.

However, not all banks are currently willing to finance oil and gas developments due to concerns about greenhouse gas emissions and the role of fossil fuels in global warming.

Some financial institutions in developed countries have become increasingly reluctant to support fossil fuel projects. Critics often point out that many of these countries historically benefited from decades of industrial development that relied heavily on fossil fuels, and that developing nations now face pressure to limit emissions while still seeking economic growth.

Despite this tension, many financial institutions continue to recognise that the global energy system cannot transition away from oil and gas overnight. For the foreseeable future, petroleum resources are expected to remain part of the global energy mix.

This does not negate the scientific consensus regarding climate change. Limiting greenhouse gas emissions remains an important global objective, and efforts to expand renewable energy, improve energy efficiency and develop advanced nuclear technologies are all part of the broader transition to lower-carbon energy systems.

The Final Investment Decision

Once the technical, financial and regulatory aspects of a petroleum development project have been prepared, the project plans are typically submitted to the host government for approval.

As a key stakeholder, the government generally reviews these proposals carefully before granting development licences or approving production permits under the relevant petroleum agreement or production-sharing contract.

Following government approval, the investing companies — often operating as a consortium — must make a final investment decision (FID). This decision formally commits the companies to proceed with the development phase of the project.

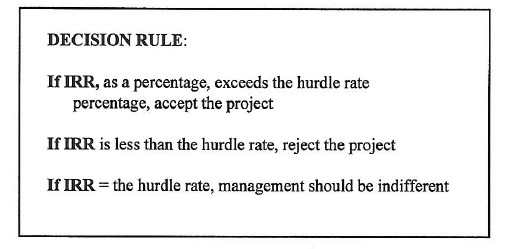

Several financial metrics are used to evaluate whether a project is suitable for investment. Traditionally, the internal rate of return (IRR) has been used to measure the expected profitability of a project by calculating the effective rate of return generated by the investment.

More commonly today, companies evaluate projects using net present value (NPV), which measures the value created by a project after accounting for the company’s required rate of return, often referred to as the investment hurdle rate.

This decision is not made by the host government but by the investing company. However, failure to proceed with development after government approval has been granted may incur severe penalties.

In many cases, the investing company is required to provide the host government with a corporate guarantee equivalent to the value of its intended investment as part of its application for development approval. This ensures that the government is not misled into approving a development that ultimately fails to proceed, allowing the company to withdraw without consequences.

When Chevron Niugini led the Kutubu Petroleum Development Project in 1990, its parent company, Chevron Corp., provided an irrevocable corporate guarantee to the Independent State of Papua New Guinea covering the value of its share of the project investment. The guarantee was issued on Chevron’s corporate letterhead and signed by the president of Chevron Corp., making it effectively as secure as cash.

Chevron proceeded with the development as planned and carried out the Kutubu project with full commitment and professionalism.